Your Money Trailguide helping you pursue your great adventure now.

Continue reading

Your Money Trailguide helping you pursue your great adventure now.

Continue reading

Quarterly update to clients

Continue reading

Latest details on the TD-Schwab merger.

Continue reading

Happy New Year! I hope this message finds you well after enjoying the holidays. I just have a quick note to share to start off our new year. A longer post will be coming later this week as our quarterly letter to clients.

2020 was a tough year on many fronts, but one thing it taught us is that market performance in the short term is wildly unpredictable. In addition, short-term performance will likely have a small impact, if any, on your probability of success with your own financial goals. So it is really not worth your mental energy to ever spend a moment worrying about your short term investment performance. Plus, none of us really have any control over investment performance.

What do we have control over? From a planning and investment standpoint, we discuss fees quite often, and look to reduce this financial headwind where possible because this is something we can control. Most of our clients have Dimensional Funds as core holdings in their portfolio, so we were happy to hear this fall that they announced that fees would be reduced across a broad range of their equity funds effective February 2021, representing an approximate 15% reduction on an asset-weighted basis. They were already significantly lower than the average mutual fund expense ratio, so this is a great move in the right direction. It is exciting because it means that, all else equal, our clients will get to keep more of the investment’s returns which will have a compounding effect on wealth over the years.

Reducing fees is only one way to increase your wealth over time. Let us know if you would like to discuss the other planning tools that can be used to increase wealth as well.

Most North Carolinian’s are working hard to take care of their families and help their neighbors in the current crisis. Nevertheless, criminals seek to exploit the Covid-19 pandemic to further their scams.

We received the notice below from the North Carolina Secretary of State warning residents to be wary, and we want to share it with you. If you or someone you care about comes across something questionable related to investing or charitable activities, please don’t hesitate to call. We can help you check it out. PLC Wealth is here to help you and answer any questions you have.

Take care, and thank you for your business with PLC Wealth.”

======================================================================================================================================

NC Secretary of State Elaine Marshall is cautioning investors that the ongoing Coronavirus pandemic will likely spark a surge of investment fraud.

“Sadly, scam artists will seek to exploit rising concerns about COVID-19 to draw people into investment traps,” warned Marshall. “Fraudsters often use the day’s headlines in their pitches, so expect to see them prey on the fear surrounding the unfolding Coronavirus pandemic and recent economic developments to promote sham investments.”

The North American Securities Administrators Association (NASAA), of which the NC Secretary of State’s Office is a member, is joining state regulators in offering tips to keep investors safe in these uncertain times.

Bad actors may develop schemes falsely purporting to raise capital for companies manufacturing surgical masks and gowns, producing ventilators, distributing small-molecule drugs and other preventative pharmaceuticals, or manufacturing vaccines and miracle cures.

Scammers also will seek to take advantage of concerns with the volatility in the securities markets to promote “safe” investments with “guaranteed returns” including investments tied to gold, silver and other commodities; oil and gas; and real estate. Investors also can expect to see schemes touting quickly earned guaranteed returns targeting seniors worried about economic disruptions and losses to their retirement portfolios.

“From guarantees of high returns without risk to promises of a miracle cures, if it sounds too good to be true, it probably is,” warned Secretary Marshall. “I urge North Carolinians to follow these tips to help protect your financial and physical health as you navigate these uncertain times.”

Investors are encouraged to call the NC Investor Hotline at (800) 688-4507 or email us at before signing over money in any investment opportunity. If you suspect an investment opportunity is fraudulent, you may report it at www.sosnc.gov. You can also find a wealth of investor education material at www.sosnc.gov/divisions/securities.

Schemes to Watch for:

Private placements and off-market securities. Scammers will take advantage of concerns with the regulated securities market to promote off-market private deals. These schemes pose a threat to retail investors because private securities transactions are not subject to review by federal or state regulators. Retail investors must continue to investigate before they invest in private offerings and independently verify the facts for themselves.

Gold, silver and other commodities. Scammers may also take advantage of the decline in the public securities markets by selling fraudulent investments in gold, silver and other commodities not tied to the stock market. These assets are often promoted as “safe” or “guaranteed” means of hedging against inflation and mitigating systematic risks. However, scammers may conceal hidden fees and mark-ups, and the illiquidity of the assets that may prevent retail investors from selling the assets for fair market value. There are no “can’t miss” opportunities.

Recovery schemes. Retail investors should be wary of buy-low sell-high recovery schemes. For example, scammers will begin promoting investments tied to oil and gas, encouraging investors to purchase working or direct interests now so they can recognize significant gains after the price of oil recovers. Scammers will also begin selling equity at a discount, promising the value of the investments will significantly increase when the markets strengthen. Never lose sight of the risks associated with any prediction of future performance and remember that market gains may not correlate with the profitability of their investments.

Get-rich-quick schemes. Scammers will capitalize on the increased unemployment rate with false promises of quick guaranteed returns that can be used to pay for rent, utilities or other living expenses.

Replacement and swap schemes. Investors should be wary of any unlicensed person encouraging them to liquidate their investments and use the proceeds to invest in more stable, more profitable products. Investors may pay considerable fees when liquidating investments, and the new products often fail to provide the promised stability or profitability. Advisors may need to be registered before promoting these transactions and legally required to disclose hidden fees, mark-ups and other costs.

Real estate schemes. Real estate investments may be appealing because the real estate market has been strong and low interest rates have increased demand. Scammers often promote these schemes as safe and secure, claiming real estate can be sold and the proceeds can be used to cover any losses. However, real estate investments present significant risks, and changes to the economy and the real estate market may negatively impact the performance of these products.

How to Protect Yourself:

The NC Secretary of State’s Securities Division offers this guidance to help investors avoid investment scams:

Ask before you invest. Investors in North Carolina should call the NC Investor Hotline at (800) 688-4507 or email us at to find out if the salesperson and the investment opportunity itself are properly registered. Investors also can check the SEC’s Investment Adviser Public Disclosure database and FINRA’s BrokerCheck. Avoid doing business with anyone who is not properly licensed. If you suspect fraud, please report it to us at www.sosnc.gov.

Don’t get hooked by a phishing scam. Phishing scams may be perpetrated by those claiming an association with the Centers for Disease Control and Prevention, the World Health Organization, or by individuals claiming to offer medical advice or services. Watch out for con artists offering “opportunities” in research and development. These scams may even be perpetrated by people impersonating government personnel, spoofing their email addresses and encouraging victims to click links or open malicious attachments. These emails may look real and sound good, but any unsolicited emails with attachments and web links may be directing you to dangerous websites and malicious attachments that can steal information from your computer, lock it up for ransom, or steal your identity. When in doubt, don’t click.

There are no miracle cures. Scientists and medical professionals have yet to discover a medical breakthrough or develop a vaccine or cure for COVID-19. Don’t fall for online pharmacies claiming to offer vaccines and don’t send money to anyone claiming they can prevent COVID-19, through a vaccine or other preventive medicine.

Avoid fraudulent charity schemes. White-collar criminals may pose as charities soliciting money for those affected by COVID-19. Fake charities will frequently use sound alike names that mimic established charities. Rather than clicking on the links or responding to the email addresses or phone numbers provided in a text, email or social media post, do an internet search to find the charity’s website and reach out to them directly. A link in an unsolicited email could send you to an impostor site. Give generously but wisely to make sure your help is going to those who need it.

Be wary of schemes tied to government assistance or economic relief. The federal government may send checks to the public as part of an economic stimulus effort. It will not, however, require the prepayment of fees, taxes on the income, the advance payment of a processing fee or any other type of charge. Anyone who demands prepayment will almost certainly steal your money. And don’t give out or verify any personal information. Government officials already have your information. No federal or state government agency will call you and ask for personal

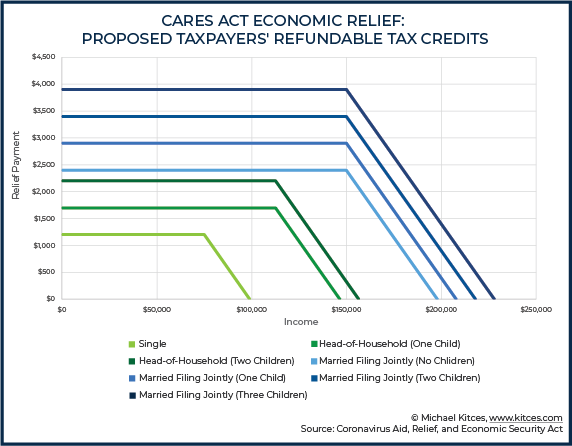

There is a good chance that you have more unscheduled time these days as almost every state in the union moves to a stay-at-home orders, but have you used this extra time to read the full H.R. 748 Coronavirus Aid, Relief, and Economic Security Act, or CARES Act? If you would rather use this newly found time in other ways, here is a time-saving summary of the CARES Act looking at 9 different provisions that may impact you. This is a longer post than normal, but is formatted so that you can scan through pretty quickly to sections that are more relevant to you. If you have any questions whatsoever, please be in touch!

======================================================================================================================================

Now you are familiar with much of the critical content of the CARES Act! That said, given the complexities involved and unprecedented current conditions, there will undoubtedly be updates, clarifications, additions, system glitches, and other adjustments to these summary points. The results could leave a wide gap between intention and reality. As such, before proceeding, please consult with us and other appropriate professionals, such as your accountant, and/or attorney on any details specific to you. Please don’t hesitate to reach out to us with your questions and comments. We look forward to hearing from you soon!

Josh, Mike, Matt, and Sandra

This will be the quarter that we look back on and never forget. It was the time that a virus spread with a silent vengeance, and the world came to a screeching halt. You may be feeling quite disoriented, fearful or even anxious as you read this note since ‘normal’ for all of us has been shaken to its core due to Covid-19. You are likely hunkering down at home, which is what you should do, with little of your regular activities to keep you busy. If you are like me, it literally feels like the earth has stopped spinning on its axis. Up is down, and right is left. Trust me when I say that it is completely normal to feel this way in the context of what we are dealing with as a human species.

I do not come to you with answers or any conclusions that will change the world…there are people that are much smarter than me working on that now, and I have confidence that they will figure it out. But I can bring some encouragement and suggest some small actions that might, just maybe, help us feel like planet earth is starting to rotate once again.

The spread of Covid-19 has impacted the global economy with a speed and impact that is unlike anything seen in our lifetime. This does not mean that happiness and contentment are totally out of your control, however. Mindset is key…start by realizing that the sun still rises every morning like the picture at the top of the article. There is new hope with each new day. I am sure you have found, as have I, that there is now more time to watch movies, read a book, take a distance-appropriate walk to enjoy the spring weather or call someone (yes, actually call them rather than text) to see how they are doing.

If you are sheltering at home with loved ones, you have probably seen them more in the last two weeks than you have for months. We should all continue to do more of these things, and the more we do, the more connected we will stay. I am not a loquacious extrovert, but I have thoroughly enjoyed being around and talking with the ones I care most about. And the more connected we stay, the more human we will feel. This is where happiness and contentment hide, not in your investment portfolio or the latest round of news.

Actions taken during times of fear in the markets will have implications for years to come. The question is whether they will be positive or negative. For the long-term investors, which are clients that we serve, volatility creates opportunity. We have taken advantage of this opportunity by tax loss harvesting, which allows us to realize the losses for tax savings, but then invest the proceeds right back in something else so the money is never out of the market. The tax savings for our clients this year will be significant. We have also looked to strategically rebalance portfolios. Because some of the fixed income assets have gains over the last year, we have sold those gains to go buy equity funds that are now at a discount. It rebalances the ship and holds to the strategy of selling high and buying low.

The fact is, I don’t know. No one does, but that’s OK. We are still waiting on the details of the massive Stimulus bill that was signed into law on March 27th. There are too many details for me to summarize here. If you want a deep dive in to the details, you can find that here. I plan to write more on this soon, but if you have any questions about this, please do not hesitate to call our office. We are all working remotely, but the extensions still ring right to us. Know that we are here to help in this time of uncertainty. Your well-being is of greatest concern to us, and not just financially. Be safe, be smart, and be part of the global solution for everyone by staying home.

We will see you soon,

Josh, Mike, Matt and Sandra