Where Things Stand

The first quarter of 2026 tested the patience of even the most disciplined investors. A combination of rising energy prices, geopolitical uncertainty, and a pullback in the large technology companies that led markets higher in recent years produced the worst quarterly performance for U.S. stocks since 2022. The S&P 500 declined approximately 4.6% for the quarter, the Nasdaq Composite fell roughly 7.1%, and the Dow Jones Industrial Average dropped in similar fashion. Meanwhile, the Russell 2000 index of smaller domestic companies held up notably better, finishing the quarter roughly flat. At the sector level, energy was the clear standout, posting its best quarterly gain on record as oil prices surged. These numbers are a useful reminder that diversification across asset classes, market capitalizations, and sectors continues to serve long-term investors well, even when individual parts of the market come under pressure. It is very difficult to capture the value in diversification if you are holding individual stocks.

Much of this quarter’s volatility was driven by the conflict in the Middle East. The war in Iran and disruption around the Strait of Hormuz sent oil prices sharply higher, contributing to renewed inflation concerns and creating uncertainty across global markets. Brent crude posted its largest monthly percentage increase on record during March, and the ripple effects were felt well beyond the energy sector. As the quarter drew to a close, reports emerged suggesting that both U.S. and Iranian leadership may be open to ending hostilities, and markets rallied meaningfully on the final trading day of March. Whether that optimism translates into a lasting resolution remains to be seen. No one knows with confidence how current geopolitical conflicts or trade disruptions will ultimately play out, and reacting emotionally to that uncertainty is rarely helpful for long-term investors. For a useful overview of how Q1 unfolded across the major indexes, Reuters published a helpful summary via U.S. News & World Report.

Why Staying the Course Matters

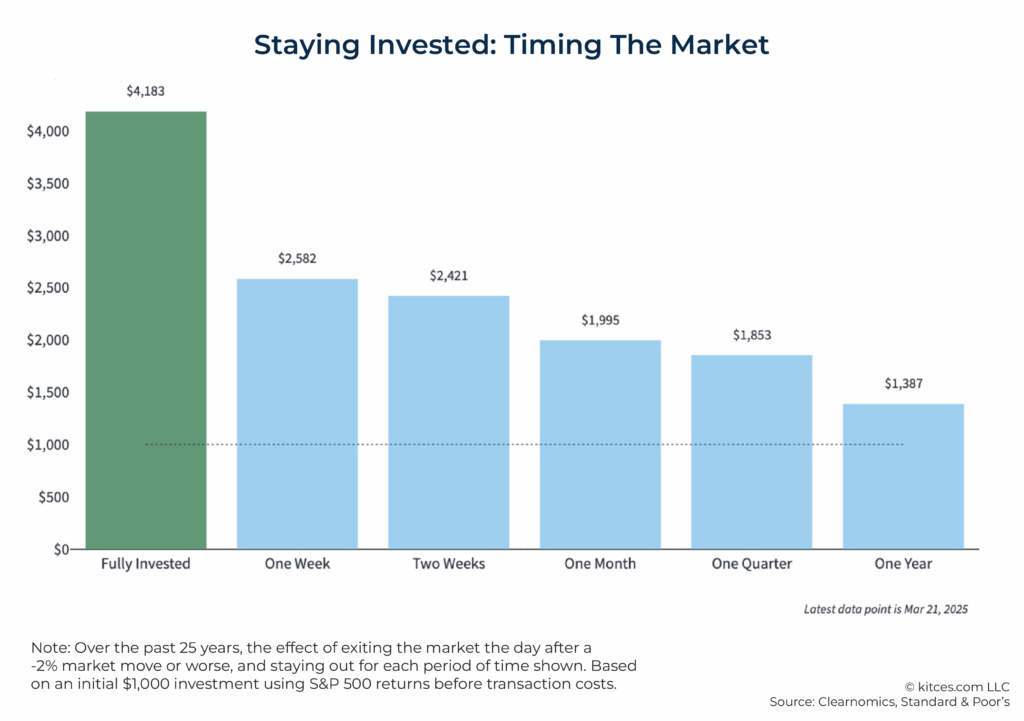

Markets are forward-looking. By the time a recession, policy shift, or geopolitical event becomes front-page news, much of that information is often already reflected in prices. This is one reason why making portfolio changes in response to headlines can be counterproductive. A diversified portfolio is designed with uncertainty in mind. Consider that the S&P 500 has now posted a negative first quarter in back-to-back years, yet history shows that a down first quarter has been followed by a positive full year far more often than not. Markets have historically moved through wars, recessions, political change, and crises while continuing to reward disciplined long-term investors over time. There is no proven way to consistently time the market, and missing even brief periods of strong performance can meaningfully affect long-term outcomes. For investors interested in the historical context around negative first quarters and what tends to follow, Motley Fool published a thoughtful analysis at fool.com.

For that reason, we will not adjust portfolios in response to market whims or short-term movements. Short-term declines do not necessarily lead to down years, and many years with significant intrayear drops have still finished with positive calendar-year returns. In fact, one of the most notable themes of Q1 was the divergence in performance across different parts of the market. While large-cap technology names bore the brunt of the selling, small-cap domestic companies in the Russell 2000 were largely insulated from the geopolitical disruption, and the energy sector delivered exceptional returns. This kind of rotation is exactly what a well-diversified portfolio is built to capture. Staying invested and focused on the long term helps ensure you are in position to benefit when markets recover and leadership shifts.

Planning Opportunities

Market turmoil can still serve a useful purpose if it prompts a review of the things that actually matter. Short-term market moves are not, by themselves, a reason to change a well-constructed long-term allocation. But when your life changes, it may be appropriate to revisit your financial plan. Retirement timing, spending needs, charitable goals, liquidity needs, estate intentions, and tolerance for risk can all justify thoughtful updates. If your plan still aligns with your values, goals, and time horizon, staying the course is often the most appropriate response.

Periods like this can also create planning opportunities worth evaluating in the context of your broader strategy. Depending on your circumstances, volatility may create room for disciplined rebalancing, tax-loss harvesting, cash-flow review, or future Roth conversion planning.

What Your Plan Is Really For

Most importantly, we would encourage you to focus on living your great life right now. Your financial plan is not meant to compete with your life; it is meant to support it. Even in periods of turmoil, your plan should prepare for important transitions, care for the people you love, and continue making progress toward the life you want to live. That may mean spending meaningful time with family, protecting time for travel or rest, supporting a cause that matters to you, or simply being more present in your day-to-day life. The headlines matter, but they are not the whole story. A well-built plan allows you to keep perspective and remember what your money is for in the first place.

As always, we are here to help you think through decisions in the context of your long-term plan rather than the emotion of the moment. If anything in your life has changed, or if you would like to revisit your plan together, please reach out.