As we close the fourth quarter of 2025 and step into a new year, I want to take a moment to reflect – not just on markets and portfolios, but on the purpose behind the plan itself.

Quarterly statements naturally draw attention to short-term market movements. They are part of the story, but never the whole story. At Ridgeline, our work together has always been grounded in a longer view: helping thoughtful, capable people design financial lives that support not only security, but meaningful experiences along the way.

Many of you I would describe as Everyday Explorers – people who take responsibility seriously, but who also want to remain curious, engaged, and fully present in your lives. Financial planning, done well, should make room for both.

The Market Backdrop: Q4 2025

The final quarter of 2025 reminded investors of a familiar truth: markets are dynamic, unpredictable, and often uncomfortable in the short term.

U.S. equities experienced continued volatility as investors weighed inflation data, evolving Federal Reserve policy, geopolitical uncertainty, and questions around economic growth. Leadership rotated within the market, sentiment shifted quickly, and headlines offered no shortage of reasons to feel either optimistic or uneasy depending on the day.

This kind of environment can test confidence – especially if investing is viewed as a quarterly scorecard. But volatility is not an anomaly. It is a feature of markets, not a failure of them. Uncertainty is not a flaw in the system – it is the system. The real question is not whether volatility exists, but whether your plan is built to withstand it.

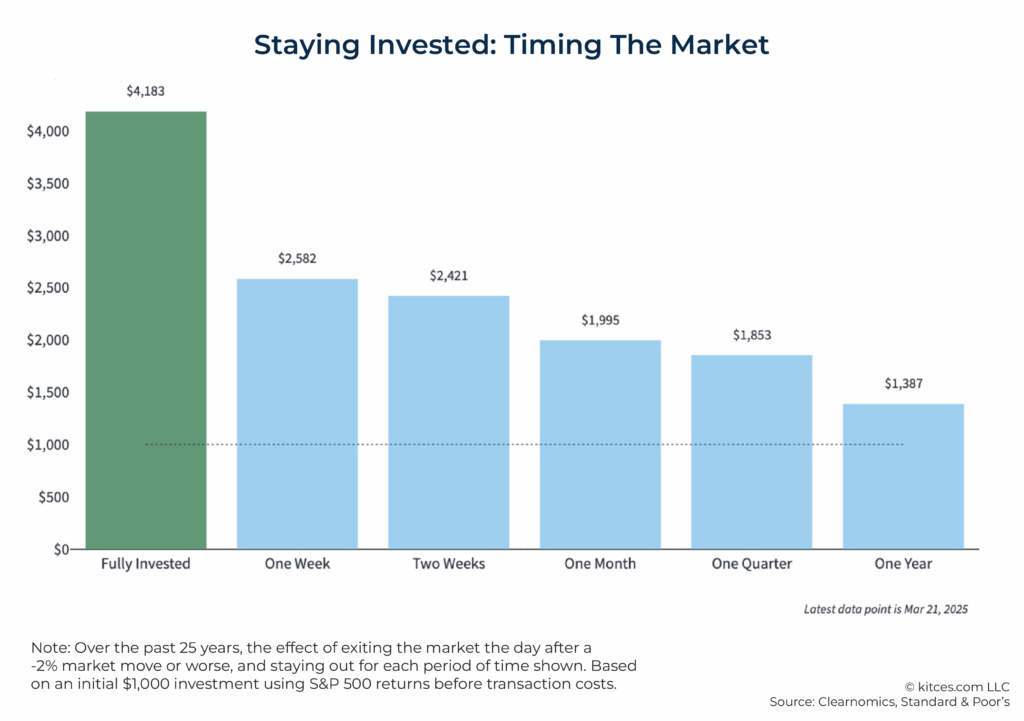

Why We Don’t Chase Returns or Predictions

One of the most important principles I want to reinforce – especially during uncertain periods – is that investment decisions should never be about chasing returns or predicting where markets will go next.

No one can consistently forecast short-term market outcomes. Acting as though we can often lead to unnecessary stress, poor timing decisions, and behavior that undermines long-term success.

Instead, our planning framework begins with a different foundation: ensuring that your future liabilities are matched or offset with safe, liquid resources.

When near-term spending needs, lifestyle costs, and known future obligations are covered by appropriate reserves and conservative assets, the long-term investment portfolio can do its job without interference. Growth assets are then free to compound over time, through inevitable cycles of optimism and uncertainty.

When this structure is in place, year-to-year market movements become background noise rather than a source of anxiety.

Planning With Intention – and With Life in Mind

One of the themes I continue to emphasize with clients is that planning should support living now, not just preparing for later.

For Everyday Explorers, that often means intentionally building room for travel, time away, outdoor pursuits, family experiences, and personal challenges that make life richer and more memorable. These experiences don’t happen accidentally. They require planning, margin, and clarity.

This is why our conversations extend beyond investments. Cash flow, liquidity, tax strategy, and risk management all play a role in creating the flexibility to say yes to meaningful experiences when the opportunity arises.

Tax and Planning Updates

As we move into 2026, several changes in the tax and legislative landscape are worth noting. Recent federal budget and benefits legislation is beginning to affect real-world planning decisions, including:

- Adjustments to retirement contribution limits and age-based catch-up provisions

- Ongoing evolution of required minimum distribution rules and inherited account timelines

- Shifting income thresholds that affect deductions, credits, and phase-outs

- The approaching sunset of certain prior tax provisions, increasing the importance of multi-year planning

None of these changes require reactive decisions. They do, however, reinforce the value of proactive coordination – aligning tax strategy, investment structure, and lifestyle goals well before deadlines appear.

Staying Grounded in What We Can Control

Market volatility tends to pull attention toward what we cannot control: headlines, forecasts, and short-term performance.

Your plan, however, is built around what is controllable:

- Spending and savings decisions

- Liquidity for known obligations

- Asset allocation aligned with time horizons

- Risk exposure that reflects your goals and temperament

- A disciplined, long-term approach

When these elements are aligned, the plan does not rely on perfect market conditions to succeed. It relies on preparation, patience, and perspective.

Looking Ahead

As we enter the new year, my commitment to you remains unchanged. I will continue to approach planning through the lens of your life, not quarterly market noise. We will continue to design plans that prioritize resilience over prediction and flexibility over optimization.

Most importantly, we will continue to use money as it was intended to be used: as a tool that supports security, opportunity, and a life well lived along the way.

Thank you for your trust and partnership. I look forward to our upcoming conversations and to navigating the road ahead together.